The 17th century bubble that foreshadows AI's fate?

What the tulip mania teaches us about bubbles

Like many people, I had heard of the tulip mania: how 17th-century traders literally swapped bulbs for an Amsterdam canal house. But I never understood why people would pay so much for just a flower bulb. Is it simply supply and demand? Or were they crazy idiots?

Before we judge them, look at the world now. In the past two decades, we have experienced several bubbles: At the turn of the millennium, the Dot-Com burst, the 2008 Crisis of Credit, more recently NFTs, and, currently, potentially, AI. To better understand why humans get caught up in such hysteria, the 400-year-old tulip mania offers a three-ingredient recipe.

The arrival of the flower

The roots of the tulip reach back to Central Asia. The flower departed from the valleys of the Pamirs and Tien Shan mountains, on the border of Afghanistan, Russia and China. By the 10th century, traders had pushed it into Persia. After a few regime changes and half a millennium later, the Ottomans in present-day Turkey appreciated its beauty and started to cultivate it. With some twists and turns, after a few decades, the Dutch noticed it too, and the flower was taken to the Netherlands in the 1590s.

Soon after arrival, the Dutch started to experiment with breeding, imitating the Ottomans. The challenge to make varieties even more beautiful than their predecessors was embraced by many. White tulips with red accents were very much sought after, and when such a crossing emerged, they would be traded for an increasingly higher value.

However, that initial trade was reserved for privileged tradesmen or nobles throughout Europe. Beyond displaying them in their gardens, elite Parisian femmes would wear them as corsages to galas, attracting eyes to their décolleté.

Such exquisite flowers continued to be traded, and the increasing prices seemed like the result of limited supply and demand with deep pockets. If so valuable, why wouldn’t they just breed more fancy coloured tulips, then?

Well, the fact that the parent bulb was of a desired colour didn’t always guarantee that the offspring would be too. Why? Because the amazing colours sought after were caused by a virus, rather than a genetic aspect, which was much less predictable. This botanical insight, nevertheless, was only discovered after the boom had busted. In short, the virus kept the fancy tulip supply limited, but the price didn’t fully skyrocket here.

The foundations of the bubble

The price stagnation was partly caused by some inherent properties of tulips. You can trade the bulbs for only three months per year; the rest of the year, they need to remain in the ground. That meant nine months of non-trading, limiting price growth.

To combat this, the innovative Dutch merchants—who invented stock market capitalism a few decades prior—started trading futures avant la lettre. Such a paper slip required you to buy bulbs when they were ready to be removed from the soil. This unlocked a dangerous new dynamic: you often didn’t need to pay the full price upfront. Only when the bulb was removed from its soil was the money due.

Therefore, such contracts were risky: you didn’t know if the bulb would be the one you were promised. That had two causes: one, people could just be fraudulent. But second, tulip’s offspring are not always guessed correctly, due to that unpredictable virus.

With these shifts, the foundations for a bubble were laid. The capital of entry was reduced, and the transactions were uncoupled from a bulb-reality.

The blowing of the bubble

To create the contracts, traders paid a third-party facilitator a small fee, called wijngeld (wine money). The name reveals a curious part of the story. These trades didn’t happen in the Amsterdam Stock Exchange, but in the smoky taverns of nearby cities, where Haarlem and Leiden played a main role. The wijngeld referred to what the money would immediately be used for.

The entry fee was quite low, roughly the price of ten to eighty pints of beer (a few stuivers or a gulden or two). This attracted a new species of traders: skilled artisans, weavers, and tradesmen of the Netherlands, who had a tradition of saving money and being opportunistic. With the tulip, they saw a chance to make a quick buck. Before, bulbs were mostly traded by botanists and the merchant elite who had spent at least some time understanding the varieties. Now, the low fees flooded the market with buyers without the relevant knowledge.

In this frenzy, a substantial portion of the trades were mere contracts. Some historians have shown trade-chains of dozens of transactions between traders, with each swap of the paper slip, the price goes up, and up.

This is how the boom accelerated onwards to one bulb being sold for close to 10.000 guilders. To put that in perspective, the average Dutch urban home at that time cost 1000 guilders. There are no records of actual Amsterdam canal houses being traded, but a few transactions did involve a house and a farmhouse. Therefore, while the trade for an actual canal house is likely an urban myth, 10000 guilders could buy you a prime one, maybe two.

The burst of the bubble

Because the people were trading in paper realities of uncertain bulbs, the transactions themselves were mostly based on the speculation that the tulip price would go up. At some point, after papers exchanged hands ten times, there was not so much factual grounding of the price beyond the fact that it would be worth more tomorrow. This worked as long as the market believed it. The only thing that could stop the bubble is when the self-fulfilling prophecy breaks. And one day, it did.

In a tavern auction in Haarlem, the auctioneer announced the price of a relatively normal bulb, a Switser (Swiss). The reaction: silence; no bids. Even when he went lower, nobody bought the tulp that would’ve been snatched in a heartbeat the day before. Slowly, people realised what was happening, and soon the news spread throughout Haarlem: the tulip trade was dead. You can imagine the staggering amount of outstanding debts.

The aftermath

Contrary to popular belief, the bust had very limited effects on the national economy. Most of the trades happened in unregulated taverns rather than on the stock markets. Instead of being backed by actual currency, the long paper chains had no money behind them. Yes, some individuals lost their life savings, but the consensus among historians today is that the macroeconomic impact was minimal.

To fix the problem of outstanding debts—long story short—most of the debts were annulled, or a law was proposed that people could buy off their debt for 3.5% of the price. However, the state of Holland ignored the proposal and suspended all outstanding deals; in Haarlem, they sometimes settled between 1%-5%.

Furthermore, the actual non-future tulip trade didn’t stop. The initial, elite trade in highly expensive bulbs continued. The layman wasn’t trading these to begin with. It’s almost as if two separate markets existed that hardly interfered with each other.

In summary, the tulip mania became a bubble because of three ingredients. One, the transactions got completely uncoupled from the actual product. Two, the influx of unregulated, unbacked capital in the form of paper slips. Three, the only basis for these transactions was the speculation that prices would rise. The moment that chain of belief breaks, the bubble bursts.

Fast forward to 2000 and onward

The tulip provides us with three ingredients which explain many bubbles we have seen in the past two decades, and the current AI one. For starters, the influx of uncertain capital. The future tulip trading echoes in the 2008 housing market crash. In this crisis, people with insufficient capital income were given mortgages they were too likely to default on, caused by poor regulations. Thus, insufficiently backed capital entered the market. Similarly, the tulip purchase contracts were an unregulated form of financing, where most laymen would not be able to pay the actual bulb price.

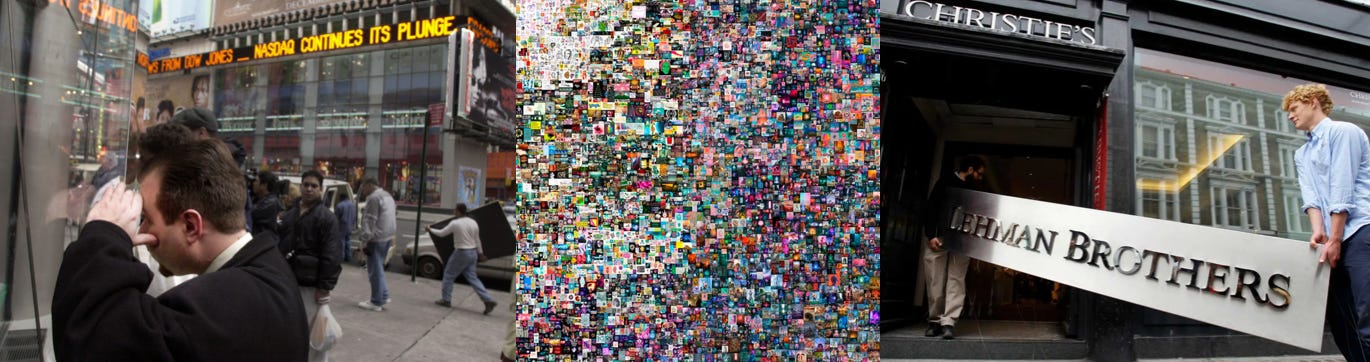

The next culprit, the uncoupling of transactions to realities, arises when comparing the bulbs to NFTs. The NFT bubble peaked when some ‘rights to a JPEG’ went for the record price of $69M. Today, that NFT is worth about $50k, according to some. NFTs, as many have pointed out, have no relationship to any reality. Those are purely speculative assets, and therefore more prone to bubbles.

The next ingredient is the cascading effect of the chain of belief breaking down. The Dot-Com bubble is a prime example. VCs pumped money into the new internet companies, but the substantial profits never materialised. When shareholders took notice, a selling frenzy occurred. On one day, the high-tech NASDAQ composite lost 10% of its value. Over the next two and a half years, this would end up losing 75% of its value, going from 5000 points to 1114 in 2002. Is AI bubble-proof?

Is AI a bubble?

There indeed is a lot of capital being pumped into that industry, mostly from VCs. Indeed, it’s better regulated than the taverns, but still, these investments hinge on the assumptions of great future results. How are these companies doing, economically?

Of course, Nvidia is doing great, but as many point out, that company is selling shovels. Turning to companies building on that infrastructure, right now, it looks like the unit economics of most AI companies are not sound.

Looking at OpenAI’s valuation, compared to its current profitability, shows a big gap between speculation and reality. The same can be said about Anthropic or Lovable, the latter of which ironically published an article this year on “How to Turn a Hobby Into a Profitable Business”.

VC money is massively funding tokens and, therefore, the adoption of AI, just like VC money gave us cheap Ubers or DoorDash meals. Obviously, there are profitable companies that build on that VC money, which have developed tooling that generates value for customers. I believe most of us have experienced the value of AI.

It’s mostly the business model, and more specifically the revenue model, and to be pedantic, the unit economics, that currently don’t make sense yet. However, prices may drop, and when they do sufficiently, the companies can rake in the profits and slowly pay back the investors, just like Uber did after 10 years or Spotify after 17 years.

To make all the bets worthwhile, and for costs to go down, some are advocating for more data centres and computing power. Economies of scale might fix the unit economics. While the lobby grows, people like Zuck are calling for it. Such lobbies are just another bet in the chain of investment, echoing the paper slips of the tulip, which we know don’t come without a risk.

For the Dot Com bubble, those bets laid much of the internet infrastructure we rely on today. For AI, it could be the same, or it could turn out that in two decades a new innovation hits (perhaps quantum computing, although that seems early), which renders all those investments obsolete.

The stark parallel is that out of hundreds of dot-com invested companies, eBay and Amazon are two of the big ones that survived—Yahoo isn’t doing so great. Which of the current AI companies will live on? Furthermore, the infrastructure was mostly laid out by the hegemonic telecom companies and public funds, not VC money. The question is not so much if AI is a bubble: it has all of the signs of a bubble. The ultimate question lies in the burst’s timing and the damage if it does.

If the AI chain of belief breaks, the main question is which stakeholders in that chain will take the biggest hit? With the tulip mania, most debts were annulled, and the effects were limited. The 2008 crisis had a more profound effect on society that still can be felt today, hurting not just companies but also ‘regular people’. These two extremes paint the spectrum of possible scenarios. Nobody knows for sure what will happen, but that massive funding can’t be sustained for more than a couple of years. The time for AI is ticking.

I owe a great debt for this story to Mike Dash’s book Tulipomania. It’s a great book that gives you more detail and very rich descriptions of what the history of the trade actually was like. Dash is an exquisite writer, and I can totally recommend this read.

Excellent read! I remember the Airplane Game was popular some decades ago. People, you have their best interests at heart, but when it comes down to it... incorrigible!